Actual Cash Value (ACV)

Cost of replacing damaged or destroyed property with a comparable new property, minus depreciation and obsolescence. For example, a 10-year-old sofa will not be replaced at current full value because of a decade of depreciation.

Additional Living Expenses (ALE)

Coverage that pays additional expenses when a policyholder has to move out of the residence while repairs are made, as a result of damage caused by a covered loss. This is also referred to as Loss Of Use.

Air Mover

(Turbo Air Mover, Fans, Dryers)

A specialized type of fan that promotes evaporation of moisture by design. Air movers incorporate an electric motor, fan and specially designed shape and housing to promote rapid drying of carpets, pad, subflooring, walls and framing members. They are also used for drying under cabinets and other hard to reach areas.

Anti-Fungal

Anti-fungal and anti-microbial refers to the prevention of the growth and spreading of fungi (mold) and its spores. This often involves the use of solvents or chemicals applied to building materials for the prevention of such growth.

Base Flood Elevation (BFE)

The computed elevation to which floodwater is anticipated to rise during the base flood. Base flood elevations are shown on Flood Insurance Rate Maps (FIRMs) and on the flood profiles. The BFE is the regulatory requirement for the elevation or flood proofing of structures. The relationship between the BFE and a structure’s elevation determines the flood insurance premium.

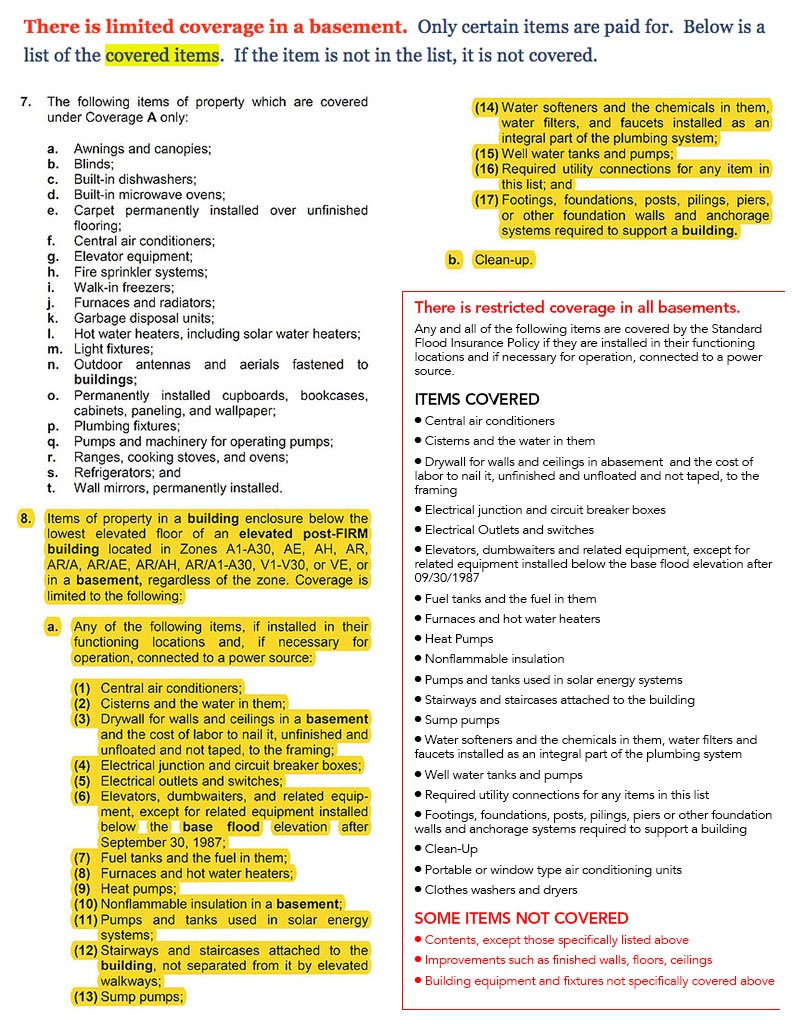

Basement

Any area of the building, including any sunken room or sunken portion of a room, having its floor below ground level (subgrade) on all sides. Click here to see what is and is not covered in a basement.

Deductible

Amount of loss that the insured pays before the insurance kicks in. The bigger the deductible, the lower the premium charged for the same coverage.

Dehumidifier

A mechanical device that promotes the reduction of moisture in the air. These devices when used properly with air movers, greatly reduce the amount of time taken to dry structural building materials, thereby greatly reducing the risk of unwanted microbial growth.

Depreciation

A decrease in the value of property due to wear, age or other cause. See Actual Cash Value above.

Described Location

The location where the insured building(s) or personal property are found. The described location is shown on the Declarations Page.

Dwelling

A building designed for use as a residence for no more than four families or a single-family unit in a building under a condominium form of ownership.

Endorsement

Endorsements can alter, delete or add coverage to an insurance policy.

Elevated Building.

A building that has no basement and that has its lowest elevated floor raised above ground level by foundation walls, shear walls, posts, piers, pilings, or columns.

Exclusions

Items or conditions that are not covered by the general insurance contract.

Flood

Flood, as used in this flood insurance policy, means:

1. A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (at least one of which is your property) from:

2. Collapse or subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined in A.1.a. above.

Homeowners Insurance Policy

The typical homeowner’s insurance policy covers the house, the garage and other structures on the property, as well as personal possessions inside the house such as furniture, appliances, and clothing, against a wide variety of perils including windstorms, fire and theft. The extent of the perils covered depends on the type of policy. An all-risk policy offers the broadest coverage. This covers all perils except those specifically excluded in the policy. There is NO Coverage for Flood in your Homeowners Policy.

Improvements

Fixtures, alterations, installations, or additions comprising a part of the insured dwelling or the apartment in which you reside.

Insured to Value (ITV)

The amount of insurance written on the property is approximately equal to its value. An insured most always want to ensure all property to value. See Underinsurance.

Increased Cost of Compliance (ICC)

Coverage for expenses that a property owner must incur, above and beyond the cost to repair the physical damage the building actually sustained from a flooding event, to comply with mitigation requirements of state or local floodplain management ordinances or laws. Acceptable mitigation measures are elevation, flood-proofing, relocation, demolition, or any combination thereof.

Institute of Inspection Cleaning and Restoration Certification (IICRC)

The IICRC is a non-profit organization devoted to the certification and standard setting for the flooring inspection, floor covering, specialized cleaning and disaster restoration industry. It aims to set the standards within these industries and promote ethics, effective communication, and technical proficiency. Aside from its role as a governing body, the IICRC also provides and disseminates information to maintain productive and fair recommendations throughout the industry. This is done to provide protection for the consumers, workers in the industry, and the environment.

Like, Kind and Quality

Like, kind and quality refer to a condition in insurance policies that states that the insurance company would cover the cost of repairing or replacing a covered loss with property similar to the original in composition and quality. As an example, flood waters damaged your laminate flooring which was installed 10 years ago. The exact laminate flooring may no longer be available. Styles, designs, materials and manufacturing processes change over time. The policy pays to replace this item with a comparable laminate flooring available today.

Limits

The maximum amount of insurance that can be paid for a covered loss. This can be found on the Declarations page of your policy.

Loss of Use Insurance

This is the same as Additional Living Expenses (ALE). Compensation for loss caused because the policyholder has lost the use of his property. Your flood policy DOES NOT cover Loss of Use or ALE.

Mildew

A coating or discoloration on moist surfaces due to molds or fungi is called mildew.

Mitigate

Mitigate means to lessen or compensate for a previous event that had a significant impact on a structure or area.

Molds

Molds are a form of fungi, which are naturally occurring in nature. These microorganisms produce enzymes that digest dead organic matter and help in the natural process of decomposition. However, mold infestations that occur within the home and other establishments can cause serious health risks to its human inhabitants. Molds are attracted to moisture, particularly on damp areas or surfaces, which have exposure to water damage Molds propagate through spores released through the air and lands on moisture-rich surfaces.

Mudflow

A river of liquid and flowing mud on the surfaces of normally dry land areas, as when the earth is carried by a current of water. Other earth movements, such as landslide, slope failure, or a saturated soil mass moving by liquidity down a slope, are not mudflows.

Named Perils

A specific risk or cause of loss covered by an insurance policy, such as a fire, windstorm, flood, or theft. A named-peril policy covers the policyholder only for the risks named in the policy in contrast to an all-risk policy, which covers all causes of loss except those specifically excluded.

National Flood Insurance Program (NFIP)

The program of flood insurance coverage and floodplain management administered under the Act and applicable Federal regulations in Title 44 of the Code of Federal Regulations, Subchapter B.

Notice of Loss

A written notice required by insurance companies immediately after an accident or other loss. Part of the standard provisions defining a policyholder’s responsibilities after a loss. This report is generated when you file your claim.

Other Structure

In homeowners policies, this refers to a structure located on the residence premises that is not directly attached to the dwelling structure, such as a detached garage or gazebo.

Peril

A specific risk or cause of loss covered by an insurance policy, such as a fire, windstorm, flood, or theft. A named-peril policy covers the policyholder only for the risks named in the policy in contrast to an all-risk policy, which covers all causes of loss except those specifically excluded.

Personal property (Contents)

Policy Rider

An amendment to an insurance policy that becomes part of the insurance contract and either expands or limits the benefits payable under the contract. Same as Endorsement.

Post-FIRM Building

A building for which construction or substantial improvement occurred after December 31, 1974, or on or after the effective date of an initial Flood Insurance Rate Map (FIRM), whichever is later.

Recoverable Depreciation

If your policy is a Replacement Cost Policy, then you can recover the depreciation deducted from your claim once the repairs are made. Let’s say your deductible is $1,000 and the repair estimate on your roof is for $8,000. Due to age and condition, your roof was depreciated by 50%. Your first payment from the insurance company will be $8,000 (Replacement cost of a roof) minus $4,000 (depreciation on the roof) minus $1,000 (deductible) which equals $3000. Once the repairs are made and you send proof of the repairs to the insurance company they will send you back your depreciation of $4,000. Therefore, you ‘recover’ your depreciation.

Remediation

In restoration work, remediation refers to the clean-up action used to reduce, isolate or remove contamination from home or a business establishment, thus preventing exposure of people and animals to these contaminants. Examples are flooded removal from basements or kitchens or mold remediation from drywall.

Replacement Cost Value (RCV)

The dollar amount needed to replace damaged personal property or dwelling property without deducting for depreciation but limited by the maximum dollar amount shown on the declarations page of the policy

Restoration

The process of rebuilding or reconstructing a portion of a property to its original look and structural state prior to a destructive incident such as mold growth, water damage, flooding or fire damage.

Salvage

Damaged property an insurer takes over to reduce its loss after paying a claim. Insurers receive salvage rights over the property on which they have paid claims. If the insurance company pays to replace your damaged sofa, they have the right to take possession of the sofa.

Special Flood Hazard Area

An area having special flood, or mudflow, and/or flood-related erosion hazards, and shown on a Flood Hazard Boundary Map or Flood Insurance Rate Map as Zone A, AO, A1-A30, AE, A99, AH, AR, AR/A, AR/AE, AR/AH, AR/AO, AR/A1-A30, V1-V30, VE, or V.

Stachybotrys

Commonly referred to as “black mold” (see Toxic Mold), this type of toxigenic mold is known to produce the harmful metabolite known as mycotoxins, which can cause adverse health effects for humans and animals, when exposed. Towards the beginning stages of growth, this mold appears white in color but soon becomes black.

Subrogation

The legal process by which an insurance company, after paying a loss, seeks to recover the amount of the loss from another party who is legally liable for it.

Toxic Mold

Also known as “black mold” or “toxic black mold”, are popular terms used to describe dark or black colored mold that may or may not produce toxic byproducts. These terms became highly publicized in the late 1990s and early 2000s when the potentially toxic and black colored species of mold called Stachybotrys was found at a number of properties with the occupants experiencing associated health problems. In actuality, there are only a few species of mold that are potentially harmful in the toxic sense. It’s important to note that while any mold is potentially harmful to those with allergies or who have weakened immune systems, not all mold is toxic and not all toxic mold is black. Stachybotrys is a type of mold that is considered toxic. There are also other types of molds that secrete mycotoxins that do not have a dark or “black” appearance.

Underinsurance

The result of the policyholder’s failure to buy sufficient insurance. An underinsured policyholder may only receive part of the cost of replacing or repairing damaged items covered in the policy. See Insured to Value (ITV).

Water Damage Restoration

The process of returning a property to its condition prior to when water damage occurred through the extraction and drying of any remaining water, dehumidifying inside air, cleaning and preserving any household items, applying deodorizing detergents and solvents and/or rebuilding any irreparable sections of the property.

Waterproofing

Is the process of making an area of a property, such as a roof, windows or basement water-resistant or protected from water or moisture intrusion from rain, flooding, or other environmental means by applying certain construction techniques, building materials and/or chemical treatments

{kind=link}