Welcome To My Website

Welcome To My Website

I’m Mark Pfister and if you’re at this page, then it’s likely I’ve been assigned as the adjuster for your flood claim. I will be your contact throughout the claims process. I’ve designed this site to answer most if not all of the questions you might have. You will find information on the flood claims process from the beginning to the end. The information on the website comes from my personal experience, the NFIP, FEMA, The American Red Cross, the IICRC, YouTube and various other sources. All of this information is readily available on the internet. I wanted to bring it all together in one location to help you through the flood claims process.

You should know that your Flood Policy is different than your Homeowners Policy. Items that are covered in your Homeowners Policy are not necessarily covered by your Flood Policy. While most Homeowners Policies are designed to make you ‘whole’, the Flood Policy is a basic policy designed to ‘get you back on your feet’, so to speak. I will go over these items when we meet for the initial inspection.

I want to let you know up front, that this will be a long arduous process, but we will get through it together. Below is a list of things that I feel you need to know as we get your flood claim started. Even if you don’t read through the rest of the website, please read through the items below. There is important information that you need to know. Once you’ve read through them, you can click on the box below that says, ‘Go to Home Page’.

Please read through the following information.

Complete & Submit the Flood Loss Questionnaire. Open & Read the Flood Claims Handbook. Download & Install the Contents Buddy Phone App. When done, scroll down to the bottom of the screen and click on the Home Page button to access the site.

What to do first:

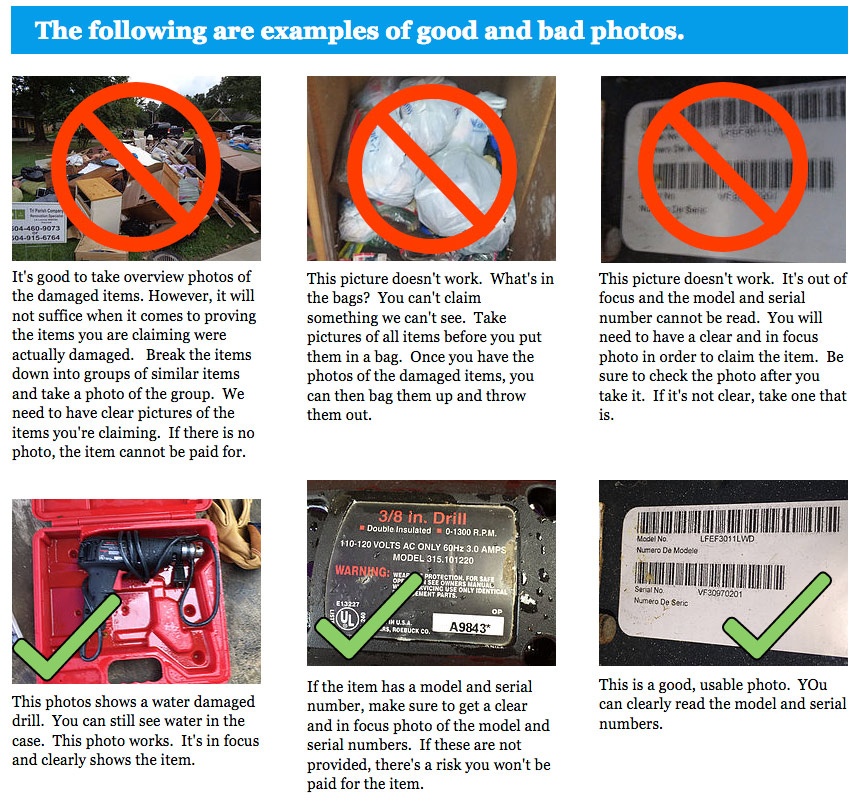

- When you get into your home, take plenty of pictures. If you’re using your cell phone, be sure to turn it sideways so the picture is wider than it is high. For an example of what your photos should look like, click here. If you’re claiming an item as flood damaged, you have to show you have it. You must show the damage to that item. If it’s not documented, it doesn’t exist. Make sure to get a clear picture of the model and serial number if the item has one or both. Please label the photo using the same name as you entered in the Contents Spreadsheet. Before you start pulling out drywall, take a photo showing the water line on the wall. You will need to put a ruler or tape measure against the wall and get a picture showing the water line along the side of the tape measure. This way we have a photo showing how high the water was in your house. Take at least one picture of each wall. If it’s a long wall with cabinets, you might need to take a few pictures. I will need these pictures to complete your estimate. If you’re not sure, take a picture.

- Don’t be in a hurry to move your contents items out of your house. Your first instinct is to drag everything out of the house and pile it on the street. Please take your time and photograph all of the items that were damaged before you throw them away. Be sure to take pictures showing the flood damage to the item. If the damage doesn’t appear to be damaged in the photo, it’s possible it will NOT be paid for. Also, if there’s not a picture of it, the policy may not pay for it. Be sure to get clear, in-focus photos of the model and serial numbers if the item has them. Please go to the Contents section of this website and read through it before you begin removing your contents. I have a few suggestions on the best way to go about removing, documenting and claiming your damaged contents.

- Download and install the Contents Buddy phone app. This app will make it much easier for you to document you flood damaged contents. By this time, you should have received and email and text from me explaining how to signup, download, install and begin using Contents Buddy. Click here to watch the video tutorials. I strongly suggest you watch the videos before you begin using the Contents Buddy phone app and website.

- Download the Flood Claims Handbook by clicking here. Please read through it. You might want to save it for future reference.

- Fill out the Flood Loss Questionnaire by clicking here. Fill in all fields and hit Submit when you’re done. This will provide information I need to get your claim started.

- Start removing the flooring and get it out of the house. If this is carpet, cut it into strips and roll up the strips. The carpet and pad will be very heavy. Only roll up the amount of carpet and pad that you can carry without hurting yourself. If tile flooring is installed on the concrete slab, do not remove it until I inspect your home. Tile installed on a concrete slab can be re-grouted, cleaned and sealed. The policy may not pay for replacing the tile installed on a concrete slab.

- Remove the drywall and insulation one foot above the water line. Take out all materials that may hold water… other than the wood studs in your walls. You cannot start the cleaning and drying process until these items are removed.

- If you hire a cleanup company, please have them call me prior to starting work on your house. Your flood policy will cover certain items in the cleanup process. I believe it’s important for the mitigation company to know what those items are so they know what can and cannot be paid for by the flood policy. The flood policy may not pay for everything they charge you for. There is a possibility you may have to come out of pocket for some of their charges.

- This will be a long process, so take your time and do your due diligence on the contractor you hire. Go to the Rebuilding page for more information on contractors.

{kind=link}